The Affordable Care Act (ACA) removed obstacles that prevented some people from buying health insurance but not everyone has signed up, and not everyone who did sign up kept their coverage. Because of that, millions will owe the individual shared responsibility payment, better known as the Obamacare penalty or ACA penalty when they file taxes.

Who pays the Obamacare penalty

The ACA’s individual mandate requires everyone in the U.S. to have health insurance unless you qualify for an exemption.

If you go more than three full, consecutive months without health insurance, you’ll pay a tax penalty for that year. If you have health insurance for only one day of a month, it doesn’t count as a month without health insurance.

Here’s an example: Say you go without health insurance for all of January and February. Then you buy health insurance and it goes into effect on the last day of March. You do not have to pay a tax penalty; you didn’t go without health insurance for three full consecutive months.

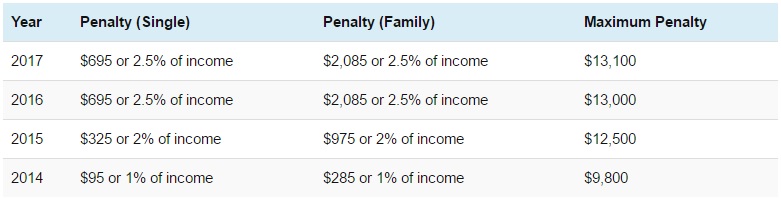

How much the Obamacare penalty costs

The penalty’s cost is calculated in one of two ways: You’ll either pay a percentage of your total household adjusted gross income — which you’ll figure on your annual tax return — or a flat rate, whichever is greater. Your tax return will also help you determine your penalty amount.

Each year, the penalty will increase to keep pace with inflation and encourage people to buy coverage.

For the tax year 2016, the penalty will rise to 2.5% of your total household adjusted gross income, or $695 per adult and $347.50 per child, to a maximum of $2,085.

For the tax year 2017 and beyond, the percentage option will remain at 2.5%, but the flat fee will be adjusted for inflation.

How to avoid the Obamacare penalty

The simplest way to avoid the penalty is by having insurance. The ACA set up the health insurance marketplace at Healthcare.gov to make this possible. There, you can search for plans and prices, or be directed to your state-specific marketplace that provides the service for your area.

Open enrollment under the ACA — during which you can sign up for coverage for the next year — only lasts for a few months. Outside of open enrollment, you may be able to sign up if you have a qualifying life event, such as a recent marriage, divorce or birth.

You don’t have to get your insurance through the marketplace, though. You can also buy coverage through your employer, a private insurer or through Medicaid if you qualify.

Some have chosen to opt-out of Obamacare, deciding that the penalty is less of a burden than buying insurance; most of them will be fined. But others may be exempt and can stay uninsured or have periods of non-coverage without facing the penalty.

Exemptions from the Obamacare penalty

If you qualify for an exemption under the ACA, you won’t be charged the penalty, even if you don’t have coverage. You could be exempt if:

- The most affordable coverage costs more than 8% of your household income.

- You were uninsured for less than three months of the year.

- You are exempt from filing a tax return because your income is too low.

- You are Native American or eligible for health services through an Indian Health Services provider.

- Your religion objects to the use of insurance.

- You’re in prison.

- You belong to a health-care sharing ministry.

- You have been abroad for more than one year.

- You qualify for a hardship exemption due to an issue such as homelessness, bankruptcy, eviction and similarly trying circumstances listed here.

If you believe you qualify for an exemption, you can claim it when you file your tax return or apply on the Healthcare.gov website.

It pays to know whether you’ll be among the millions expected to face the individual mandate penalty when filing tax returns next year. (If you file taxes online, the preparer you choose will calculate any penalty.) That will help you budget now for penalty costs. And with the next open enrollment period always around the corner, it may be time to reconsider your coverage and potential penalty for the year ahead.

How the penalty is calculated

The “Obamacare penalty” is pro-rated for the number of months you’re without coverage. It’s one-twelfth of the annual penalty amount for each month you don’t have coverage – and “having coverage” means being insured for at least one day of the month in question.

One annual gap of fewer than three months is allowed with no penalty, and there’s also a provision for handling gaps in coverage that span across two calendar years. (Note that a three-month gap in coverage would result in a penalty for all three months; the gap has to be less than three months in order to be exempt from the penalty.)

Increasing penalties

For a family of two adults and two children with a $40,000 MAGI, the individual mandate penalty for 2015 was $975 (calculated by adding $325 + $325 + $162.50 + $162.50). But if that same family had a $90,000 MAGI, the penalty was $1,388 instead, calculated as [(90,000 – 20,600) times 0.02 = $1,388] (note that the flat rate penalty results in a larger penalty at the lower-income, while the percentage of income penalty results in a larger penalty at the higher income level).

For 2016, the penalty again increased substantially; it will be assessed when 2016 tax returns are filed. Our hypothetical uninsured family of four earning $90,000 would be subject to the flat-rate penalty of $2,085 for 2016 ($695 per adult, $347.50 per child), as this is larger than the percentage of income penalty [(90,000 – 20,600) times 0.025 = $1,735]. But uninsured families with even higher incomes will be penalized 2.5 percent of their taxable income when they file their returns in early 2017.

The IRS reported in January 2016 that 7.9 million tax filers owed the penalty for being uninsured in 2014, while 12.4 million tax filers qualified for exemptions. Going forward, it’s expected that exemptions will apply more often than penalties for uninsured tax filers. But for those who are not exempt, the penalty assessed on 2016 tax returns will be quite significant.

For those who remain uninsured in 2017, the percentage of income penalty will be the same as it was in 2016, but the flat-rate penalty will be higher than $695 per uninsured adult (and the household maximum flat-rate penalty will be higher than $2,085).

Know your penalty before tax time

It’s important to be aware of how the penalty works before tax season gets here. If you don’t learn about the 2016 penalty until you file your taxes, you may find yourself stuck with a penalty for 2017 as well, because the 2017 health insurance open enrollment period will end two and a half months before the tax filing deadline for 2016 returns (open enrollment for 2017 plans ends on January 31, 2017).

The tax filing season in early 2015 was the first time that people encountered the ACA’s tax penalty on their returns. Prior to that, a significant number of people weren’t aware that they’d be penalized for not having health insurance, and in all but three states, a special enrollment period was available to allow people facing 2014 penalties to enroll in a plan for 2015.

But no such special enrollment period was granted in 2016 since people are much more aware of the fact that they have to maintain health insurance coverage in order to avoid a penalty.