A system the IRS uses to identify potentially fraudulent electronically filed tax returns. It enhances the IRS’s capabilities to detect, resolve, and prevent criminal and civil noncompliance and reduces issuance of fraudulent tax refunds.

The Return Review Program (RRP) is the Internal Revenue Service’s (IRS) primary individual tax refund fraud selection system. The RRP uses predictive analytics, models, filters, clustering, a scoring system, business rules, and selection groups to identify suspected identity theft, individual tax refund fraud, and frivolous filer tax returns. The RRP has real-time filtering capabilities and is designed to improve the IRS’s ability to detect, resolve, and prevent fraud. In addition to the RRP, the IRS uses the Dependent Database (DDb). The DDb is a rules-based system that incorporates information from many sources such as the Department of Health and Human Services, the Social Security Administration, and the IRS. The IRS initially implemented the DDb in March 2000 to identify taxpayer noncompliance, but in Processing Year (PY) 2012, the IRS added identity theft filters within the DDb system to identify potentially fraudulent tax returns involving identity theft. Finally, the IRS uses the Electronic Fraud Detection System (EFDS) as its case management system to control potentially fraudulent tax returns selected for review.

Why did my tax return get selected for Refund Review Program?

The Internal Revenue Service (IRS) faces an ongoing challenge to detect and prevent noncompliance with tax laws. Noncompliance and fraud threaten the integrity of the tax system, costing the federal government billions of dollars annually. Every year taxpayers willfully or unintentionally fail to pay hundreds of billions of dollars owed in taxes. This noncompliance includes individuals who make inadvertent mistakes and fraudsters who intentionally seek to evade taxes and obtain invalid refunds.

Identification and Verification of potentially fraudulent tax returns

During tax return processing, the IRS systemically evaluates fraud potential for both paper and electronically filed tax returns claiming refunds using both the RRP and the DDb systems. This evaluation is done prior to issuing the tax refund. For those tax returns identified as potentially fraudulent, the IRS sends the tax return to its Integrity and Verification Operations (IVO) function for tax examiner screening and verification. Specifically, tax returns with a fraud potential score above the IVO’s return review tolerance level are added to IVO inventory and are resequenced (i.e., processing of the return and any associated refund is delayed) for 14 days to allow tax examiners sufficient time to screen the return. It should be noted that if IVO tax examiners do not screen assigned returns within 14 days, processing will systemically resume for the return and the refund is released.

Integrity and Verification Operations (IVO) tax examiners can take the following actions:

- Screening – A tax examiner reviews the tax return for income and withholding information, including comparing the income and withholding information reported on the current tax year return to previous tax year returns to identify inconsistencies. For returns verified as legitimate, the tax examiner “refiles” the return (i.e., the return is considered verified as good and the refund can be released). If the tax examiner concludes that the tax return is potentially fraudulent, the related income documents are sent for verification and a refund hold is placed on the individual’s tax account. This hold gives the IRS additional time to verify the legitimacy of the tax return.

- Verification – A tax examiner uses various methods to verify income and withholding amounts reported on the potentially fraudulent tax return, including contact with the reported employer by phone or fax and reviewing internal data.

- Referral to the Taxpayer Protection Program – Tax returns meeting identity theft criteria are sent to the Taxpayer Protection Program. The refund is held while the return is reviewed by this program.

- Referral to the Scheme Tracking and Referral System – If a tax examiner verifies a tax return as false and the income and withholding amounts are within a certain dollar tolerance but there is no indication of identity theft, the return is sent to the Scheme Tracking and Referral System and a refund hold is placed on the tax account. This indicates a tax examiner determined that the return is false or partially false.

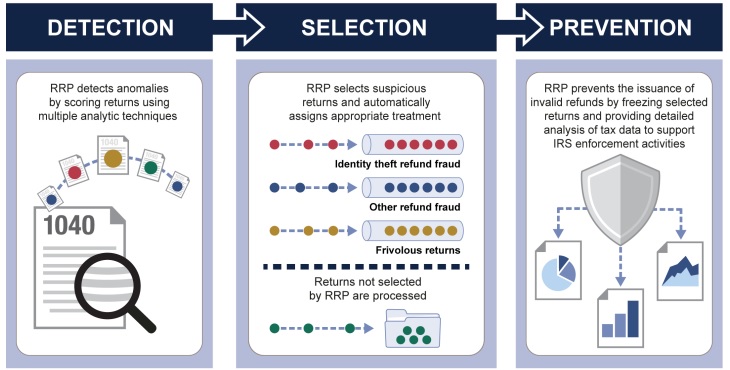

Return Review Program(RRP) performs three major activities:

Detection

According to IRS, RRP uses advanced analytic techniques and evaluates data from various sources to assign multiple scores to individual returns claiming refunds. The scores are based on characteristics of Identity Theft and other refund fraud known to the IRS. Higher fraud scores indicate the return’s greater potential for refund fraud. IRS officials have stated that RRP’s design helps IRS identify increasingly sophisticated tax fraud.

RRP’s analytic techniques include the following:

- Predictive models IRS develops many different models that help detect emerging fraud, outliers, and taxpayer behavior inconsistencies in returns claiming refunds. These models also mine data and help IRS seek out patterns predictive of IDT and other refund fraud. For example, a model may use a combination of existing variables from the 1040 individual tax return, such as tax credits claimed and income.

- Business rules RRP contains over 1,000 rules (a “yes” or “no” outcome) developed by IRS to flag returns for evidence of anomalous behavior. For example, RRP uses a business rule to distinguish between returns for which it has received an associated Form W-2, Wage and Tax Statement (W-2), from those which it has not.

- Clustering RRP uses a tool that reveals patterns and relationships in masses of data allowing RRP to identify clusters of returns that share traits predictive of schemes and refund fraud. For example, IRS could use clustering to identify groups of returns that share the same geographic location, among other traits. According to IRS, this technique was developed to automate certain aspects of Criminal Investigation’s identification of fraud schemes.

A number of systems connect to RRP and provide additional taxpayer data or third-party information for RRP to analyze. RRP contains taxpayers’ prior three years’ filing history and third parties—employers, banks, and others—file information returns to report wages, interest, and other payment information to taxpayers and IRS.

For example, the Social Security Administration sends W-2s to the IRS. The W-2 information is loaded regularly into RRP.

Selection

RRP has filters that combine results from the analytic techniques to automatically make a selection decision and then a treatment decision before the return can move to the next processing step and a refund can be issued. Returns not selected by RRP continue through the pipeline process.

- Selection decision Returns with fraud scores above thresholds—and meeting other criteria set by IRS management—will automatically be selected by RRP filters for further action or review. According to IRS, the agency’s capacity to review selected returns is part of the automated selection decision, as are other criteria that weigh the cost and risk to the IRS. IRS reports that for the 2017 filing season, RRP selected 857,438 returns as potential Identity Theft(IDT) refund fraud and 219,210 returns as potential other refund fraud. This is less than 1 percent of almost 158 million individual returns filed that year.

- Treatment decision RRP automatically assigns selected returns to the appropriate treatment based on the characteristics of Identity Theft(IDT) or other refund fraud RRP detected.

Examples of treatments include the following:

- Identity theft refund fraud Returns selected by an IDT filter are automatically assigned for treatment in the Taxpayer Protection Program. IRS notifies taxpayers that they must authenticate their identity before IRS will process the return or issue a refund. Taxpayers can verify their identity by calling an IRS telephone center, visiting a Taxpayer Assistance Center, or in some cases, authenticating online or via mail. If the taxpayer does not respond to the letter or fails to authenticate, the return is confirmed to be IDT refund fraud.

- Other refund fraud If a return is selected by one of RRP’s nonidentity theft filters, RRP automatically assigns the return, based on the characteristics of fraud identified, to the Integrity and Verification Operations (IVO) function within W&I’s Return Integrity and Compliance Services office for further action or review. For example, RRP may select a return as potential refund fraud because it is missing verification of income for a refundable tax credit, such as the Earned Income Tax Credit. IVO tax examiners may then, for example, contact employers to confirm the income and withholding amounts reported on the return.

- Frivolous returns RRP selects returns that contain certain unsupportable arguments to avoid paying taxes or reduce tax liability. If

IRS determines these returns to be frivolous, the taxpayer may be subject to penalty. RRP assigns potentially frivolous returns to IVO for review and to notify the taxpayer. - Non-workload returns RRP’s non-workload filters select returns that, according to IRS, score just below the thresholds for RRP’s other filters described above. IRS officials stated that RRP loops these returns for additional scoring and detection.

Prevention

RRP supports IRS’s efforts to prevent issuing invalid refunds in the following ways:

- Freezing refunds RRP connects directly to IRS’s systems for processing individual tax returns and issues transaction codes directly to the Individual Master File depending on the type of refund fraud RRP detected. IRS reports that for the 2017 filing season, RRP prevented IRS from issuing about $4.4 billion in invalid refunds. Of that amount, $3.3 billion was attributed to Identity Theft(IDT) refund fraud and $1.1 billion to other refund fraud.

When RRP selects a return as potential IDT refund fraud, RRP will simultaneously assign the return for treatment and issue a transaction code telling IRS’s processing systems to freeze the refund until the case is resolved. As a result, IRS can protect the refund until the review is complete or a legitimate taxpayer has authenticated his or her identity, at which point IRS will release the return.

If RRP’s non-identity theft filters select the return because of characteristics predictive of other refund fraud, RRP issues a transaction code to freeze the return for 14 days while IVO examiners have the opportunity to screen the return. After 14 days, the return automatically resumes processing and the refund may be released. Accordingly, IRS officials told us that RRP prioritizes IDT treatment and if a return is selected by both IDT and other refund fraud filters, RRP will automatically assign the return to the Taxpayer Protection Program and freeze the refund.

IRS officials stated that when RRP’s non-workload filters select a return, RRP will issue a transaction code that delays the payment of the refund associated with the return for 1 week. According to IRS officials, this delay provides IRS an opportunity to manually review returns that contain suspicious characteristics.

- Incorporating treatment results IRS integrates the results from each return review into its analytic techniques to improve RRP’s detection ability and accuracy on an ongoing basis. For the 2018 filing season, IRS officials told us they were able to add functionality that uses real-time case feedback data to automatically improve the accuracy of some of RRP’s IDT fraud filters. IRS officials can also change RRP’s selection criteria or filters during the filing season based on emerging fraud or workload concerns.

- Detailed data and analysis With RRP, all available taxpayer information is linked together and available for analysis and queries by IRS employees for post-refund enforcement activities, such as criminal investigations. RRP creates and distributes a report with the results of RRP’s clustering analysis to analysts in Criminal Investigation. IRS employees are also able to

search RRP and analyze data relevant to their specific enforcement activities. Criminal Investigation officials told us they use RRP reports to identify suspicious returns that were not selected by RRP and flag them for further post-refund review.