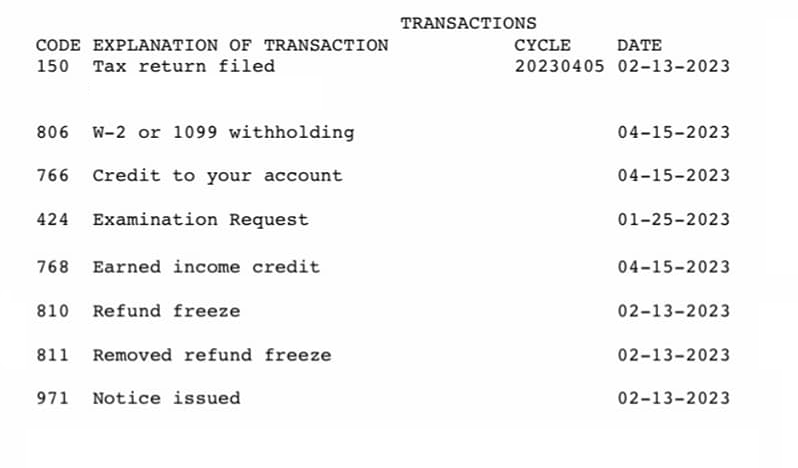

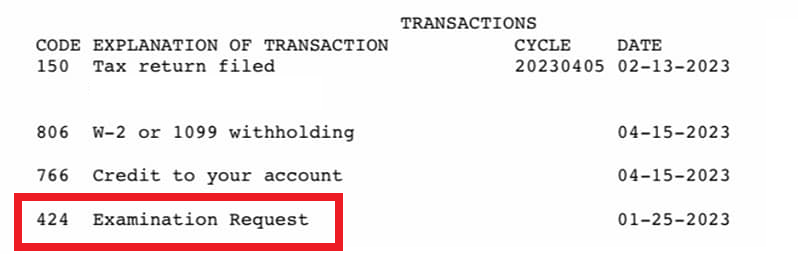

The transaction code TC 424 is an Examination Request and is the code that will appear on your tax transcript if your tax return has been referred for further examination or audit. The IRS uses this code TC 424 when a tax return is submitted to the Examination or Appeals Division. TC 424 means the IRS pulled your tax return for further examination to ensure that your reported taxes are accurate.

Selecting a tax return for examination does not always suggest that the taxpayer has either made an error or been dishonest. In fact, some examinations result in a refund to the taxpayer or acceptance of the return without change.

IRS Tax Transcript Code 424 means Request for Examination/Audit

Transaction Code 424 on your tax transcript means that your tax return has been pulled for further examination to determine if a full audit is required. You should expect a letter from the IRS asking for supporting documents or additional information related to your tax return within a few weeks.

IRS Definition Of Transaction Code 424?

Return referred to Examination or Appeals Division. Generates Examination opening inventory information. Deletes record, if present, from DIF file. This transaction can also be generated for IMF when an IRP Underreported Case is referred to Exam. Generated as a result of input through PCS.

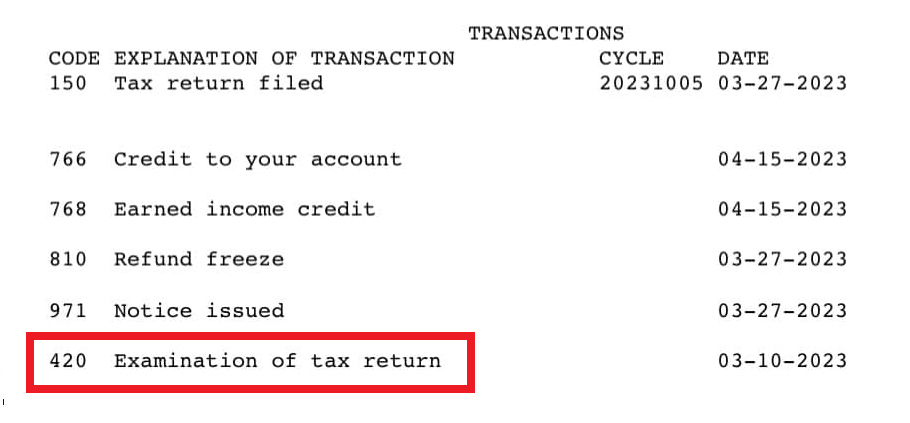

424 Examination Request could change to 420 Examination of Tax Return

The TC 424 is posted to the tax transcript when the IRS is examining your return to see if they need to audit the tax return. The Transaction Code 420 is a full audit. So if you started out with a TC 424 on your transcript and it was replaced with a TC 420 this means the IRS examiner determined that the tax return needed a full audit to ensure information is reported correctly according to the tax laws and to verify the reported amount of tax is correct.

The IRS selects to examine tax returns using a variety of methods, including:

- Potential participants in abusive tax avoidance transactions – Some returns are selected based on information obtained by the IRS through efforts to identify promoters and participants of abusive tax avoidance transactions. Examples include information received from “John Doe” summonses issued to credit card companies and businesses and participant lists from promoters ordered by the courts to be turned over to the IRS.

- Computer Scoring – Some returns are selected for examination on the basis of computer scoring. Computer programs give each return numeric “scores”. The Discriminant Function System (DIF) score rates the potential for change, based on past IRS experience with similar returns. The Unreported Income DIF (UIDIF) score rates the return for the potential of unreported income. IRS personnel screen the highest-scoring returns, selecting some for audit and identifying the items on these returns that are most likely to need review.

- Large Corporations – The IRS examines many large corporate returns annually.

- Information Matching – Some returns are examined because payer reports, such as Forms W-2 from employers or Form 1099 interest statements from banks, do not match the income reported on the tax return.

- Related Examinations – Returns may be selected for audit when they involve issues or transactions with other taxpayers, such as business partners or investors, whose returns were selected for examination.

- Other – Area offices may identify returns for examination in connection with local compliance projects. These projects require higher-level management approval and deal with areas such as local compliance initiatives, return preparers, or specific market segments.

Examination Methods

An examination may be conducted by mail or through an in-person interview and review of the taxpayer’s records. The interview may be at an IRS office (office audit) or at the taxpayer’s home, place of business, or accountant’s office (field audit). Taxpayers may make audio recordings of interviews, provided they give the IRS advance notice. If the time, place, or method that the IRS schedules are not convenient, the taxpayer may request a change, including a change to another IRS office if the taxpayer has moved or business records are there.

The audit notification letter tells which records will be needed. Taxpayers may act on their own behalf or have someone represent or accompany them. If the taxpayer is not present, the representative must have proper written authorization. The auditor will explain the reason for any proposed changes. Most taxpayers agree to the changes and the audits end at that level.

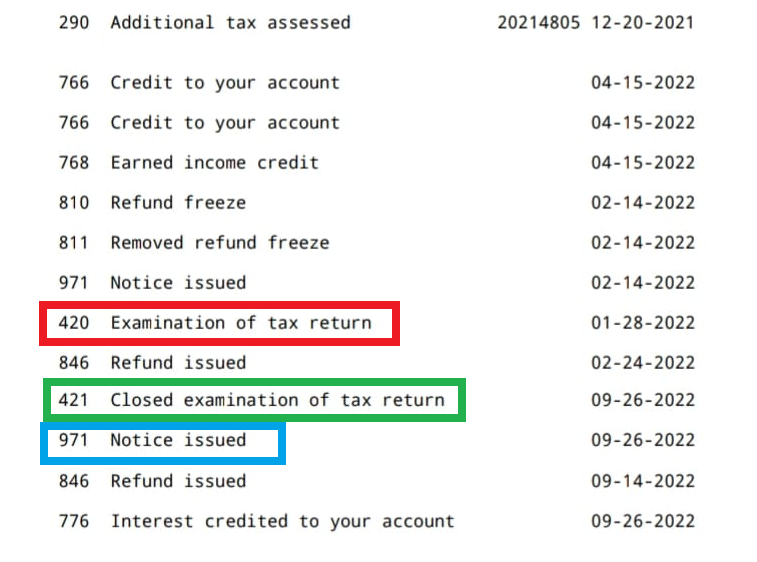

TC 421 Closed Examination of Tax Return

Once the IRS completes the examination, it may accept your return as filed or propose changes.

When the TC 421 Closed Examination of Tax Return is posted on the tax records, the TC 421 will indicate that the examination is closed and completed and the issue has been resolved.

A TC 971 code may show up indicating a notice was issued.

Tax Transcript code 971 indicates that the IRS will send you a notice or letter requesting additional information, a notice of an account change, or a notice that your tax return is being reviewed and will list the steps you need to take and the documents you will need to present to resolve the issue.

The IRS performs audits by mail or in person. The notice you receive will have specific information about why your return is being examined, what documents if any they need from you, and how you should proceed.

Appeal Rights

Appeal Rights are explained by the examiner at the beginning of each audit. Taxpayers who do not agree with the proposed changes may appeal by having a supervisory conference with the examiner’s manager or appeal their case administratively within the IRS, to the U.S. Tax Court, U.S. Claims Court, or the local U.S. District Court. If there is no agreement at the closing conference with the examiner or the examiner’s manager, the taxpayer has 30 days to consider the proposed adjustments and their next course of action. If the taxpayer does not respond within 30 days, the IRS issues a statutory notice of deficiency, which gives the taxpayer 90 days to file a petition to the Tax Court. The Claims Court and District Court generally do not hear tax cases until after the tax is paid and administrative refund claims have been denied by the IRS. The tax does not have to be paid to appeal within the IRS or to the Tax Court. A case may be further appealed to the U.S. Court of Appeals or to the Supreme Court if those courts accept the case.

Remember: If you are facing Hardship The Taxpayer Advocate Service may be able to assist some people but there are thousands of reviews needing assistance, unfortunately, the reviews are required and a taxpayer advocate can not prevent the review from being done on the return.

If you can show a true existing hardship they will try to have the review expedited but they will have to make that determination based on priority showing a true hardship, (for example, someone truly being evicted has a notice or notice that utility is being turned off with termination date, or can’t buy life-saving medication required for illness, (like insulin for diabetes as an example), etc…due to the number of people requesting taxpayer advocate assistance.